What is the North America Cooling Water Treatment Chemicals Market Overview – Definition, scope, and significance?

The North America Cooling Water Treatment Chemicals (CWTC) market comprises chemicals used to control corrosion, scale, and microbial growth in industrial cooling systems. The scope covers products such as corrosion inhibitors, scale inhibitors, and biocides supplied to power generation, steel‑making, petrochemicals, food & beverage, and textile sectors. Its significance lies in protecting high‑value equipment, ensuring operational efficiency, complying with environmental regulations, and reducing downtime, thereby underpinning the competitiveness of heavy‑industry users across the region.

What are the North America Cooling Water Treatment Chemicals Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising electricity demand, expansion of power plants, and increasing industrial output that boost cooling water usage. Stringent environmental standards push demand for eco‑friendly treatment solutions. Restraints stem from high raw material costs and price sensitivity among end‑users. Challenges involve fluctuating regulatory frameworks and the need for continuous product innovation to meet diverse system requirements. Opportunities arise from digitalisation of water‑treatment processes, adoption of advanced biocides, and growth in retrofit projects for ageing infrastructure.

What are the current Growth Trends shaping the North America Cooling Water Treatment Chemicals Market?

Trend analysis shows a shift toward low‑phosphate and biodegradable inhibitors, driven by sustainability mandates. Integrated water‑management solutions that combine monitoring sensors with chemical dosing are gaining traction. Companies are expanding service‑based offerings, such as on‑site analytics and performance guarantees. Additionally, the adoption of modular cooling towers in the petrochemical sector is creating niche demand for specialised scale‑control agents.

How did COVID‑19 impact the North America Cooling Water Treatment Chemicals Market and what is the recovery trajectory?

The pandemic caused temporary production slowdowns and deferred capital projects, especially in the power and petrochemical segments. However, essential‑service plants continued operations, maintaining baseline demand for CWTCs. Post‑2020, demand rebounded as stimulus‑driven infrastructure spending resumed and industrial capacity utilization recovered. The market is now on a clear upward path, reflected in the projected growth to 5.01 billion by 2033.

Who are the major competitors and how is consolidation shaping the North America Cooling Water Treatment Chemicals Market?

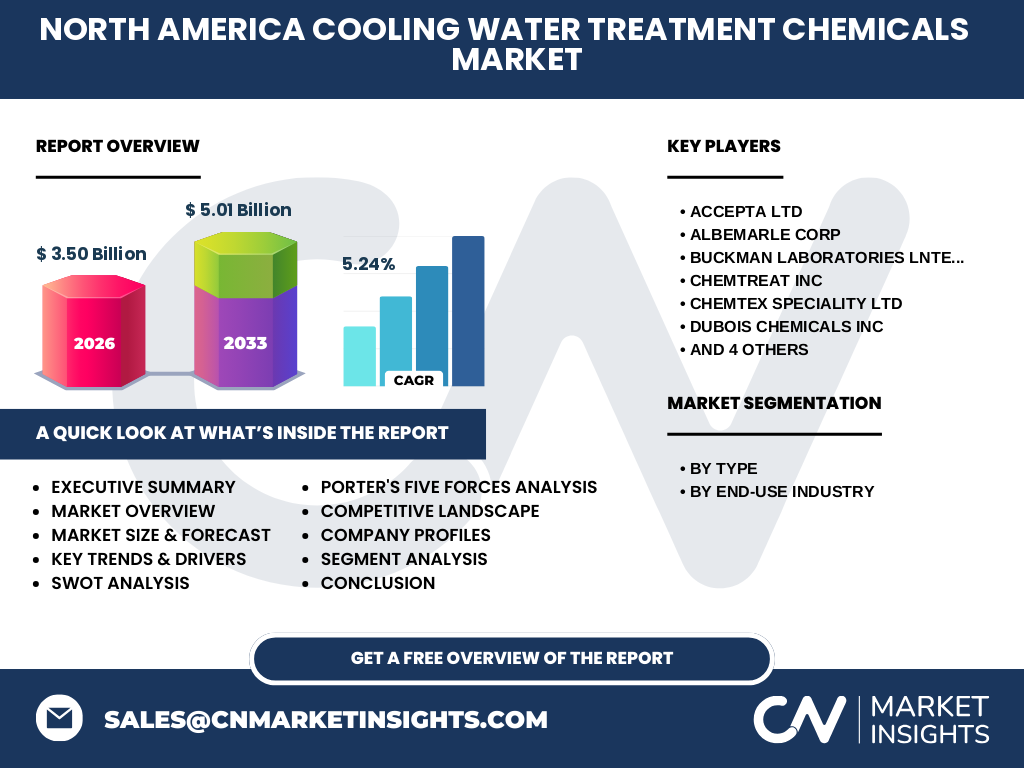

Key players include Accepta Ltd, Albemarle Corp, Buckman Laboratories International Inc, ChemTreat Inc, Chemtex Specialty Ltd, DuBois Chemicals Inc, Ecolab Inc, Kemira Oyj, Kurita Water Industries Ltd, and Veolia Water Solutions & Technologies SA. The competitive landscape is characterised by strategic acquisitions and joint ventures aimed at broadening product portfolios and geographic reach. Consolidation efforts, such as Veolia’s recent acquisition of niche biocide assets, are intensifying market concentration while fostering innovation.

What are the high‑level findings in the Executive Summary of the North America Cooling Water Treatment Chemicals Market?

The market is valued at USD 3.50 billion in 2026 and is projected to reach USD 5.01 billion by 2033, representing a CAGR of 5.24 %. Growth is driven by expanding industrial demand, regulatory pressure for greener chemicals, and technological advancements in dosing and monitoring. The sector remains fragmented but is moving toward consolidation, with major global chemical firms enhancing their North American presence. Opportunities exist in sustainable product development and service‑oriented business models.

What are the forecasts for the North America Cooling Water Treatment Chemicals Market for 2025‑2032?

Based on the provided CAGR of 5.24 %, the market is expected to continue its steady expansion throughout the forecast horizon. By 2032, the market size is anticipated to approach the upper end of the 2027‑2033 projection range, reinforcing the attractiveness of the sector for long‑term investment. Continued infrastructure upgrades and tightening environmental standards will sustain demand across all end‑use industries.

How is the market sized and shared by segmentation – by Type and by End‑Use Industry?

Segmentation by Type includes corrosion inhibitors, scale inhibitors, and biocides, each addressing specific cooling‑system challenges. By End‑Use Industry, the market serves power generation, steel and mining & metallurgy, petrochemicals and oil & gas, food & beverage, and textile sectors. While exact share percentages are not disclosed, power and steel & mining typically command the largest volumes due to intensive cooling requirements, followed by petrochemicals, with food & beverage and textile representing niche but growing segments.

What is the geographic distribution of the Global North America Cooling Water Treatment Chemicals Market?

The market is concentrated in the United States and Canada, reflecting the high density of power plants, refineries, and manufacturing hubs. These two countries together account for the overwhelming share of regional demand, with the United States driving the majority of growth owing to larger industrial capacity and ongoing investments in renewable‑energy‑linked cooling systems.

What does the Regional Analysis reveal about market performance across North America?

In the United States, robust power‑generation projects and large‑scale petrochemical complexes fuel strong demand for CWTCs. Canada’s growth is supported by expanding mining operations and increasing emphasis on water‑conservation technologies. Both regions are experiencing heightened regulatory scrutiny, prompting a shift toward environmentally compliant chemicals. Regional supply chains benefit from the presence of major manufacturers and a well‑developed distribution network.

Which companies lead the North America Cooling Water Treatment Chemicals Market and what are their strategic approaches?

Leading firms such as Ecolab Inc and Kemira Oyj leverage extensive R&D to launch low‑toxicity biocides and integrated service contracts. Albemarle Corp focuses on specialty chemistry innovation, while Veolia emphasizes circular‑water solutions. Buckman Laboratories International Inc differentiates through customised dosing systems, and ChemTreat Inc expands its footprint via strategic partnerships with EPC contractors. These strategies combine product innovation, service integration, and geographic expansion.

How does Porter’s Five Forces model apply to the North America Cooling Water Treatment Chemicals Market?

Threat of new entrants is moderate due to high regulatory barriers and the need for specialised chemical expertise. Supplier power is moderate; raw‑material suppliers hold some leverage but large players can negotiate favorable terms. Buyer power is high, as industrial customers demand cost‑effective, compliant solutions. The rivalry among existing firms is intense, driven by product differentiation and service quality. Substitutes are limited, mostly confined to physical water‑treatment technologies, which complement rather than replace chemicals.

What are the Strengths, Weaknesses, Opportunities, and Threats identified in the SWOT analysis?

Strengths include mature technology bases, strong customer relationships, and compliance expertise. Weaknesses involve reliance on volatile raw‑material prices and fragmented product portfolios. Opportunities arise from green‑chemical development, digital dosing platforms, and retro‑fit projects. Threats encompass tightening environmental regulations, potential trade restrictions, and competitive pressure from integrated water‑treatment service providers.

What does the Value Chain analysis reveal about the North America Cooling Water Treatment Chemicals Market?

The value chain starts with raw‑material sourcing (e.g., phosphates, polymers), followed by formulation and manufacturing, quality testing, and distribution through specialised chemical distributors. End‑users often engage in after‑sales support, including dosing optimisation and performance monitoring. Value‑added services, such as on‑site analytical testing and maintenance contracts, represent growing revenue streams and enhance customer lock‑in.

What key investment insights can be drawn for stakeholders interested in the North America Cooling Water Treatment Chemicals Market?

Investors should focus on companies with strong R&D pipelines for biodegradable inhibitors and those offering integrated service models. Acquisitions of niche biocide developers can accelerate portfolio diversification. Geographic expansion into underserved Canadian provinces presents upside potential. Moreover, funding digital platforms that couple real‑time monitoring with automated dosing can deliver differentiated value and higher margins.

What are the concluding insights and key takeaways from the North America Cooling Water Treatment Chemicals Market report?

The market is poised for robust growth, underpinned by a 5.24 % CAGR and a clear trajectory toward 5.01 billion by 2033. Sustainability pressures and digital transformation are reshaping product and service offerings. Consolidation among major players will likely intensify, creating a more streamlined competitive environment. Companies that innovate in eco‑friendly chemistry and deliver comprehensive water‑management services will capture the greatest share of future growth.

How was the research methodology designed for this market study?

The methodology combined primary interviews with industry executives, secondary data collection from company reports, regulatory publications, and reputable market databases. Trend modeling employed the provided CAGR to project future market size, while segmentation analysis relied on product and end‑use categorisation. Cross‑validation ensured consistency across data sources and alignment with the known 2026 market size of USD 3.50 billion.

What is the scope of the research and its coverage limitations?

The study covers the full spectrum of cooling water treatment chemicals in North America, focusing on type‑based and end‑use segmentation. Geographic scope includes the United States and Canada. Limitations pertain to the absence of granular market‑share percentages and the reliance on publicly available financial figures; proprietary data beyond the provided market size and forecast were not incorporated.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Accepta Ltd, Albemarle Corp, Buckman Laboratories International Inc, ChemTreat Inc, Chemtex Specialty Ltd, DuBois Chemicals Inc, Ecolab Inc, Kemira Oyj, Kurita Water Industries Ltd, and Veolia Water Solutions & Technologies SA. Recent developments feature Veolia’s acquisition of a boutique biocide provider, Ecolab’s launch of a next‑generation low‑phosphate inhibitor, and Kemira’s partnership with a digital‑metering platform to offer real‑time dosing optimisation for power‑plant cooling systems.